Today’s top story: What parents and students need to know about financial aid. Also in the news: Using your smartphone or tablet to clean up your finances, tax tips for procrastinators, and what to do when your teenager has become a financial disaster.

Today’s top story: What parents and students need to know about financial aid. Also in the news: Using your smartphone or tablet to clean up your finances, tax tips for procrastinators, and what to do when your teenager has become a financial disaster.

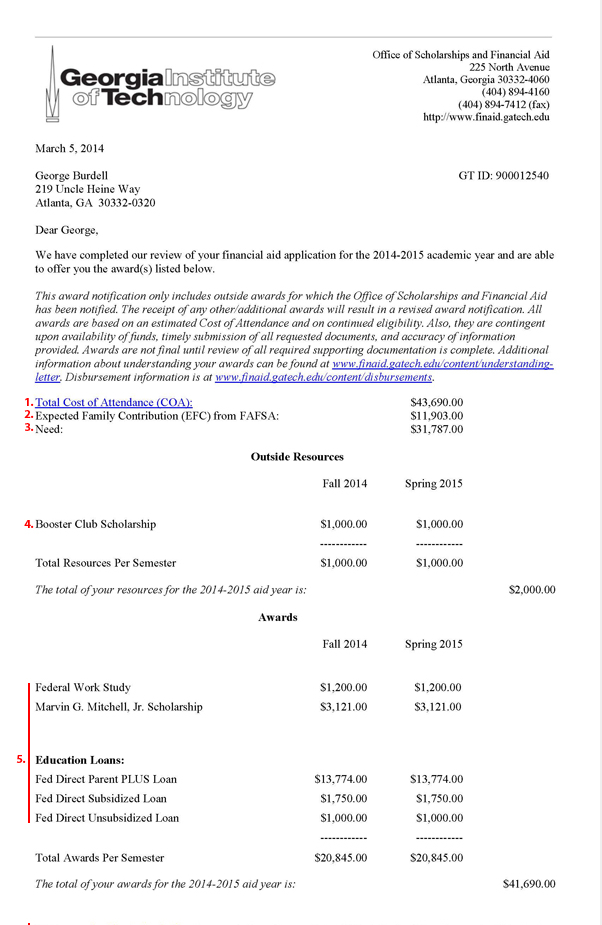

Eight Financial Aid Secrets That Parents And Students Need To Know

What you need to know before filling out the FAFSA.

12 Powerful Ways Data Can Help Clean Up Your Finances

Putting your smartphones and tablets to work.

6 tax tips for procrastinators

Tick-tock.

Help! My Teen is a Money Monster

What to do when your kid is out of financial control.

How to Budget For Health Care Expenses in Retirement

Health care expenses will eat up a significant part of your retirement savings.