If you want to see what’s wrong with many financial aid letters today, check out the one that Georgia Institute of Technology has so helpfully posted on its Web site under the rather ironic headline “Understanding the Letter.”

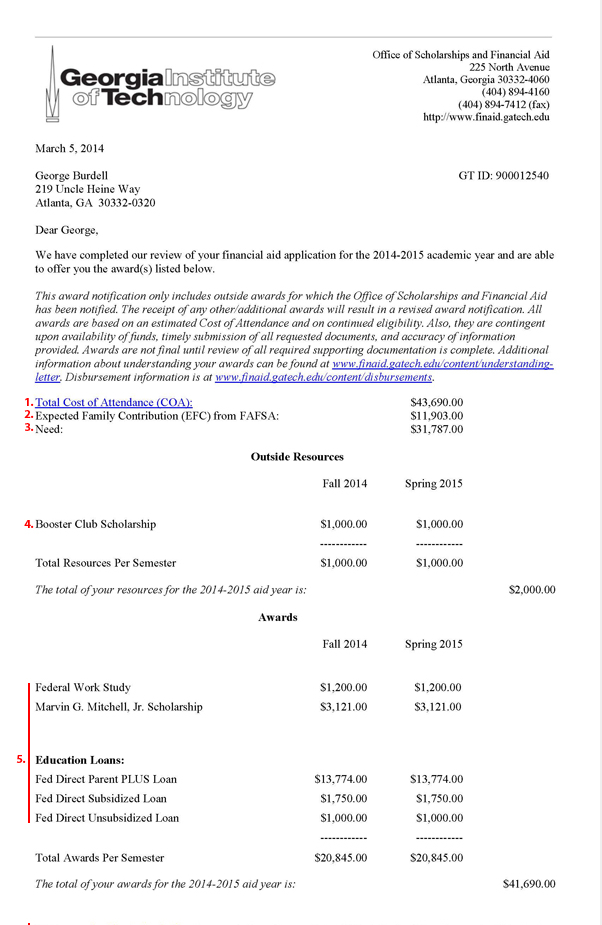

The school does a few things right. Not all colleges include the total cost of attendance on their financial aid letters, and many don’t include the “expected family contribution”–what the family is expected to pay according to the Free Application for Federal Student Aid or FAFSA. Subtracting the expected family contribution from the total cost results in the family’s need. In this case, the need is $31,787.

The school does a few things right. Not all colleges include the total cost of attendance on their financial aid letters, and many don’t include the “expected family contribution”–what the family is expected to pay according to the Free Application for Federal Student Aid or FAFSA. Subtracting the expected family contribution from the total cost results in the family’s need. In this case, the need is $31,787.

The total award figure of $41,690 seems dazzlingly generous compared to the family’s need. It’s not.

Like many schools, GIT lumps together gift aid (scholarships and grants) with loans and work study.

In this case, the gift aid is just $8,242, which includes a $2,000 scholarship the student won on his own.

The vast majority of the “aid”–$27,548–are parent PLUS loans. PLUS loans are designed to help the family pay its expected contribution, which in this case is $11,903. PLUS loans don’t reduce the family’s $31,787 need.

This award that seems so generous actually meets a quarter of the family’s actual need with gift aid. When work study and the student’s loans are included, the percentage of need met is only about half.

Too many financial aid letters are even more obscure, as I write in this week’s Reuters column, “Don’t get fooled by financial aid letters.” Some don’t include any cost information, while others list partial information. Some don’t spell out what’s a loan and what’s not. Fewer than half of schools use the federal “Shopping Sheet,” which was designed to help stop misleading financial aid letters and allow families to compare aid offers. You can find the sheet here, and using it to parse letters like this can really help you understand how generous–or not–a college is actually being.