We had a great Twitter chat today about preparing financially for college, hosted by Experian. (You’ll find the tweets using #creditchat.)

We had a great Twitter chat today about preparing financially for college, hosted by Experian. (You’ll find the tweets using #creditchat.)

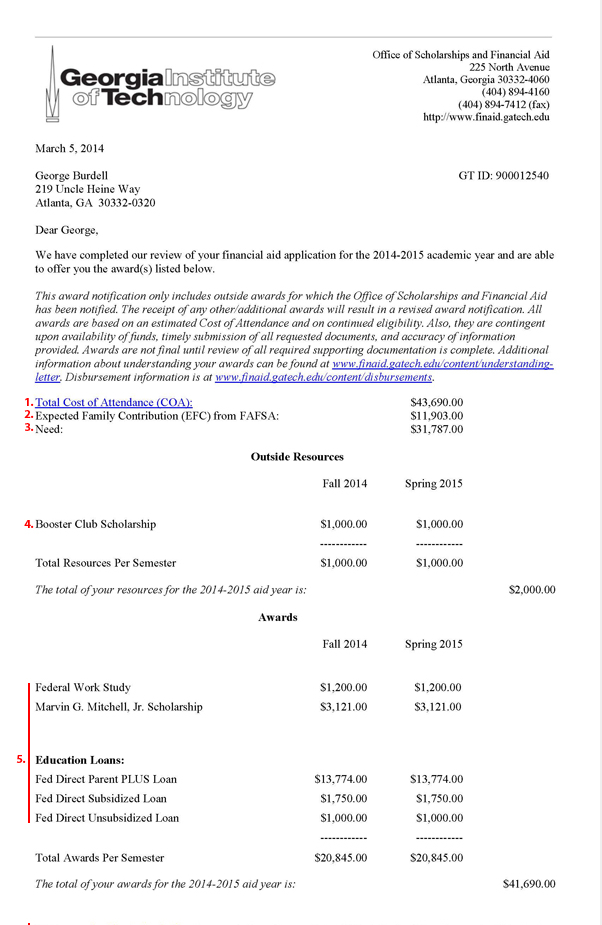

I was distressed, though, that many believe people should look for scholarships as a way to reduce college costs. That’s not how it usually works.

If you have financial need, colleges typically deduct the amount of so-called “outside” scholarships from the free aid such as grants and their own scholarships that they otherwise would give you. Schools don’t have to reduce the loan portion of your package unless your outside scholarships exceed the grants and other free aid they were planning to bestow.

They’re not just being mean. It’s what federal financial aid rules require, according to FinAid. If you don’t have financial need, outside scholarships could reduce the merit aid a school would otherwise give you.

Does that mean you shouldn’t search and compete for outside scholarships? No. But it’s certainly not a reliable solution to the college affordability problem.

A better approach for students and families is to look for generous schools. Colleges themselves are the greatest source of scholarships, but most don’t meet 100 percent of their students’ financial need. Some meet 70 percent or less. If you want a better deal, look for schools that consistently meet 90 percent or more of their students’ need. College Board and College Data are among the sites that can help you find this information.