The more you understand about how credit works, the more frustrated you get with how much misinformation is floating around out there. At least, that’s true for me and the three experts who joined me last week on a Google hangout to talk about “Credit myths that need to die.”

The more you understand about how credit works, the more frustrated you get with how much misinformation is floating around out there. At least, that’s true for me and the three experts who joined me last week on a Google hangout to talk about “Credit myths that need to die.”

John Ulzheimer, who’s worked at Equifax and Fair Isaac, has unique insight into the credit reporting world. One thing that drives him around the bend is the persistent myth that employers use credit scores to evaluate applicants. Another myth he hates: the one about how closing accounts hurts your credit scores.

Gerri Detweiler, who writes for Credit.com and runs the DebtCollectionAnswers.com, discusses how medical debts affect your credits and debunks the myth that you need to carry balances to improve your credit scores.

Maxine Sweet heads consumer education at Experian and battles the myth that there’s just one credit score.

Take some time today to check out our discussion. You’ll come away from it a lot more informed about credit and how to make yours the best.

If someone is being denied a job because of bad credit, does it really matter that much, from their point of view, whether it’s because of their credit REPORT or their credit SCORE? I totally understand and sympathize with how someone who’s an expert in this area could be “driven around the bend” by persistent errors in terminology by the media, but as far as ordinary consumers are concerned, it seems like a distinction without a difference.

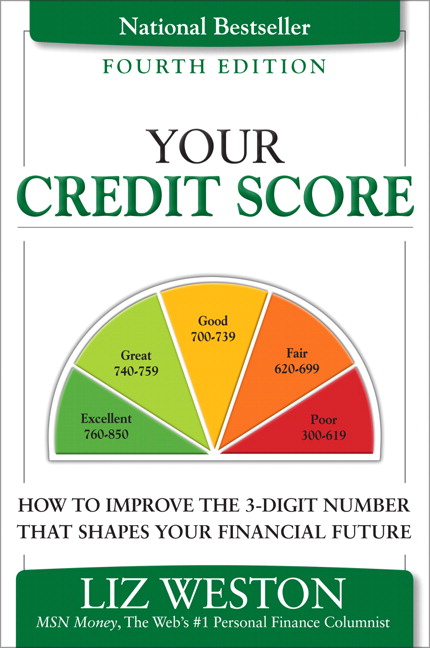

I’d say there are some significant differences. A single skipped payment, for example, can knock more than 100 points off a good credit score. An employer reviewing a credit report likely would barely take note of that. What they’re looking for are more serious indicators of financial trouble, such as chargeoffs and collections. (That said, there’s no evidence that credit and job performance or honesty are in any way correlated.) At the very least, when you hear someone using credit scores and reports interchangeably, you have a good indicator that the person doesn’t know much about credit reporting and shouldn’t be relied on for information about how it works.