Today’s top story: How the way you think about money could be hurting your finances. Also in the news: Determining the right time to buy a home, six secrets to getting a good deal on that home, and why your FICO score is about to look very different.

Today’s top story: How the way you think about money could be hurting your finances. Also in the news: Determining the right time to buy a home, six secrets to getting a good deal on that home, and why your FICO score is about to look very different.

3 Money Maxims that Hurt Your Finances

Changing the way we think about money.

When Should You Wait to Buy a Home?

How to determine when the time is right.

6 secrets to getting a good deal on a house

Tips for when the time is right.

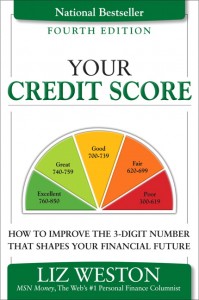

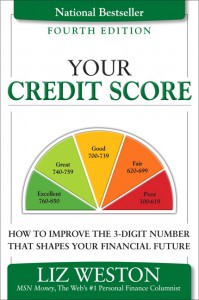

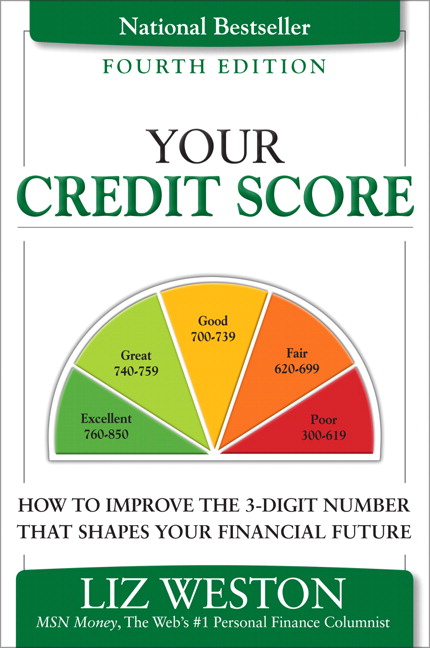

How credit scores are about to change: a Q&A

Your FICO score is about to get a makeover.

Why it’s easier to rob bitcoins than banks

Not that you should do either one, of course.